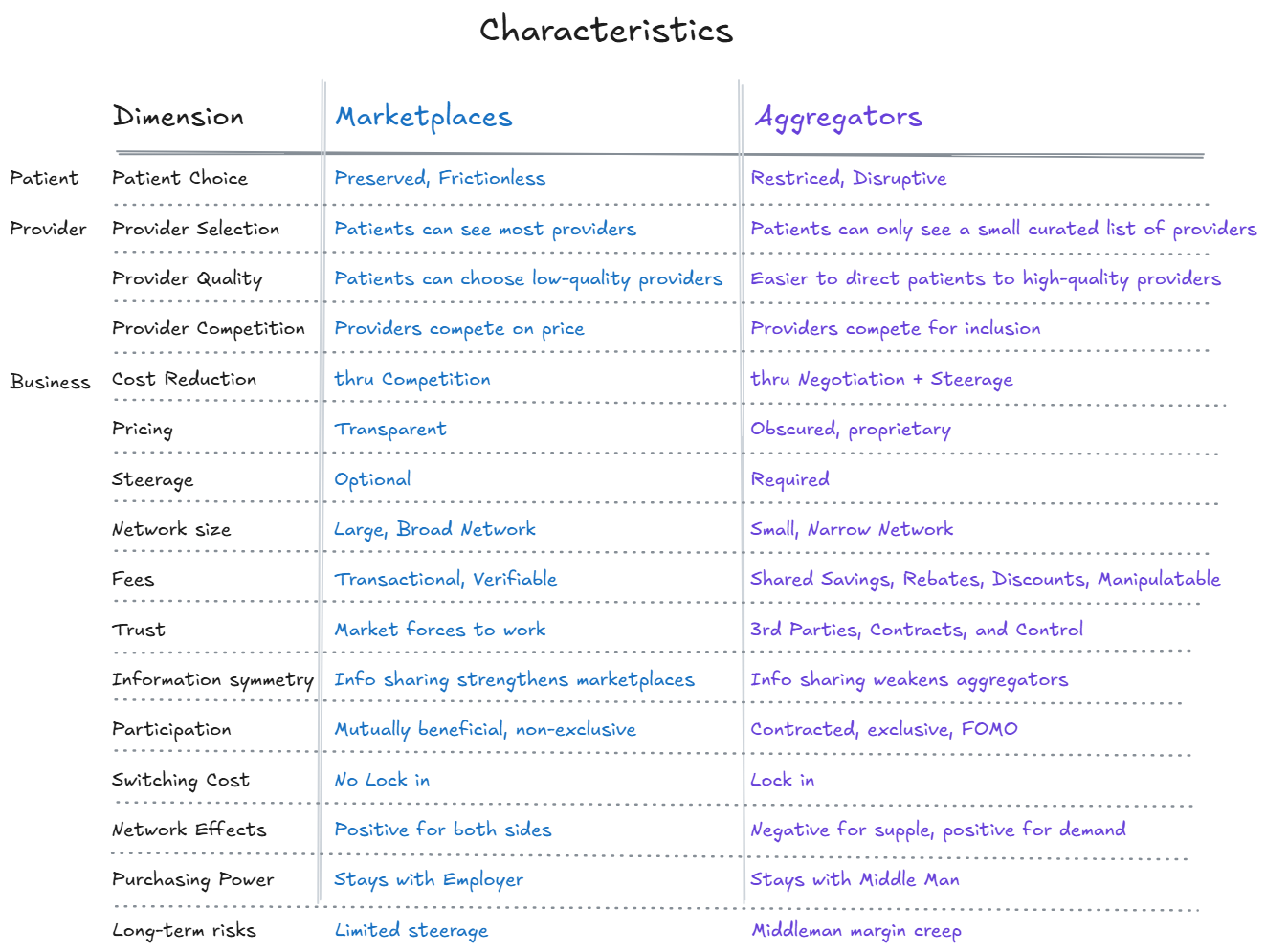

Purchasing Surgical Bundles with Marketplaces vs. Aggregators

Self-insured plan sponsors (employers) are purchasing surgical bundles through both marketplaces or aggregators. Both marketplaces and aggregators are middlemen that help plan sponsors (i.e., demand) find high-quality surgeons (i.e., supply) who are willing to offer lower prices in return for more patient volume. Both marketplaces and aggregators negotiate surgical bundle rates, handle claims and payments, and sometimes provide care navigation (active routing systems).

Despite these similarities, marketplaces and aggregators have almost orthogonal business strategies, which will be the main topic in this article. Are these middlemen providing a useful service to disrupt the broken fee-for-service system and lower costs, or are they just another middleman who will extract more value out of the healthcare system than they provide?” Lastly, we will discuss other areas of healthcare with marketplace and aggregator business strategies (teaser: PBMs are aggregators).

Surgical Bundle Aggregators

Surgical Bundle Marketplaces

Creating Surgical Bundles

In order for provider organizations to sell surgical bundles, they must first create the surgical bundles by bundling the surgeon’s fee, the anesthesiologist’s fee, the facility fee, the implant fee, and the rehab fee into one surgical bundle price. The provider organization must be capable of receiving payment from the marketplace and distributing the appropriate payments to the facility, anesthesiologist, and rehab locations, which is a substantial barrier for many provider organizations.

Marketplaces

Marketplaces encourage all provider organizations to post their bundle prices on the marketplace and do not directly influence the bundle price. Marketplace bundles can be for routine clinic visits, MRI, PT, and/or surgical services.

Marketplaces are non-exclusive, so all physicians can participate in the marketplace. In fact, the marketplace actively recruits physicians because more physicians mean a stronger network. The larger, non-exclusive networks mean patients are more likely to be able to see their preferred provider.

Marketplaces achieve lower bundle prices through supply competition. Physicians compete on price, access, and/or quality. Marketplaces could actively steer patients to high-quality, less-expensive providers, but most marketplaces rely on the plan sponsors’ third-party care navigators to actively route patients to the most appropriate physician. Marketplaces improve when more providers and patients transact on the marketplace because there are positive network effects for both sides. More providers attract more patients, and more patients attract more providers. More transactions provide more quality data, which increases everyone’s trust in the marketplace. Marketplaces do not promise providers increased patient volume. Providers must earn their patient volume through competitive prices, good quality, and better access.

Marketplaces charge a transactional percentage fee (~10% of the bundle price) that is transparently disclosed on their marketplace for all parties to see. Marketplaces succeed when supply and demand have relatively equal market power, and competitive market forces should result in appropriate pricing of bundles. Marketplaces thrive when both supply (providers) and demand (plan sponsors) are provided with price and quality data and trust that data. More information means more trust, which means more transactions. Supply and demand will only transact on the marketplace when it is mutually beneficial to them. There is no contractual obligation for either side to participate in the marketplace or limitation from participating in another marketplace. There is no “lock in.” Therefore, the marketplace must provide value and trust to both sides (plan sponsors and physicians). Plan sponsors maintain control of how they purchase healthcare. Plan sponsors can change aspects of their benefits (third-party administrations and/or care navigation companies) and maintain their relationship and data with the marketplace. Marketplaces teach plan sponsors how to purchase surgical bundles instead of being a middleman that secretly does it all for them.

Aggregators

Aggregators negotiate on behalf of multiple plan sponsors to obtain lower rates for surgical bundles. Aggregators amass a critical volume of patient lives (i.e., demand) and then negotiate with a limited number of physicians (i.e., supply) for lower surgical bundle rates in exchange for exclusive access. In exchange for guaranteed patient volume through exclusivity, patient steerage, and first-dollar coverage, some providers will accept these lower rates. Aggregators typically provide narrower networks where patients are given a limited choice of providers and cannot always choose their preferred physician. Many quality providers may remain out-of-network with aggregators because the narrow network helps the aggregator negotiate lower rates (FOMO).

Aggregators do not attempt to provide whole MSK care. They are interested in the big-ticket items (surgery) where their active routing and care navigation can achieve the largest savings. Often, a patient will begin their MSK care with an out-of-network MSK physician. That out-of-network physician will make a diagnosis and may recommend surgery. When the request for prior authorization for surgery is sent to the carrier, the aggregator is notified and contacts the patient to inform them of their plan benefits. The patient’s co-pay for surgery is typically waived if the patient selects the aggregator’s preferred physician for their surgery.

The terms of the negotiated contracts between the provider organizations and the aggregator are not typically shared with the plan sponsors. Therefore, employers have information asymmetry about how the providers are selected and must place their trust in the aggregator to negotiate the best bundle prices and select the best quality providers on behalf of the employer. Aggregators have done a better job than marketplaces at identifying quality providers, but in the future, they could use quality scores as a justification to narrow their network even further. Narrow networks help aggregators standardize and coordinate patient care since there are fewer providers to manage. IMHO, most physicians (~75%) provide quality outcomes. The gains from improving physician quality are mostly achieved by removing the bottom quartile of providers from the network and not by selecting just the top quartile of providers in the network. (For more information about how most physicians do good work and why sports teams rarely repeat championships, read my previous blog, The Paradox of Skill.)

Aggregators typically charge a shared saving fee, which is a percentage of the difference between a reference price and the actual price of the surgical bundle. The reference price could be the plan sponsor’s historic cost for a particular surgery or the price of a surgical bundle in the patient’s location. Aggregators could charge additional disclosed or undisclosed fees for care navigation, physician credentialing, and/or data processing.

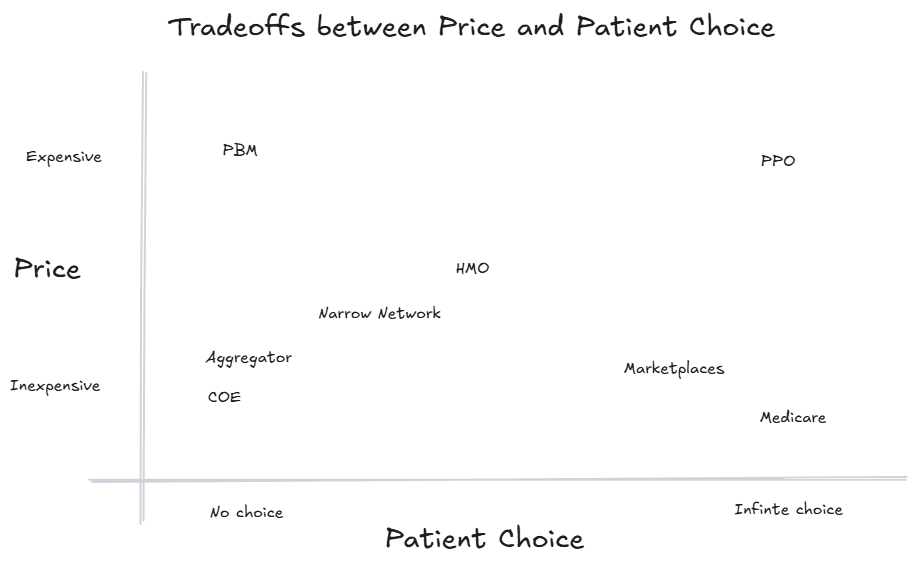

Price vs. Patient Choice

In healthcare, there is often a trade-off between price and patient choice. In a PPO plan, patients can see most providers but pay a higher premium. HMOs narrow the network of available physicians but extract better rates from their select providers and lower the patients’ premiums. The most extreme narrow network is probably Walmart’s centers of excellence program that required elective cardiac and orthopedic surgeries to be performed at 4-5 centers. When the centralized negotiating agent has more authority (i.e., exclusivity), they can generate greater savings by sacrificing patient choice. The two obvious exceptions to this trade-off between price and patient choice are PBMs and Medicare. Medicare provides inexpensive care with maximum patient choice through governmental power. PBMs have convinced everyone that the procurement of medications is so complicated that it is impossible to buy medications without a PBM.

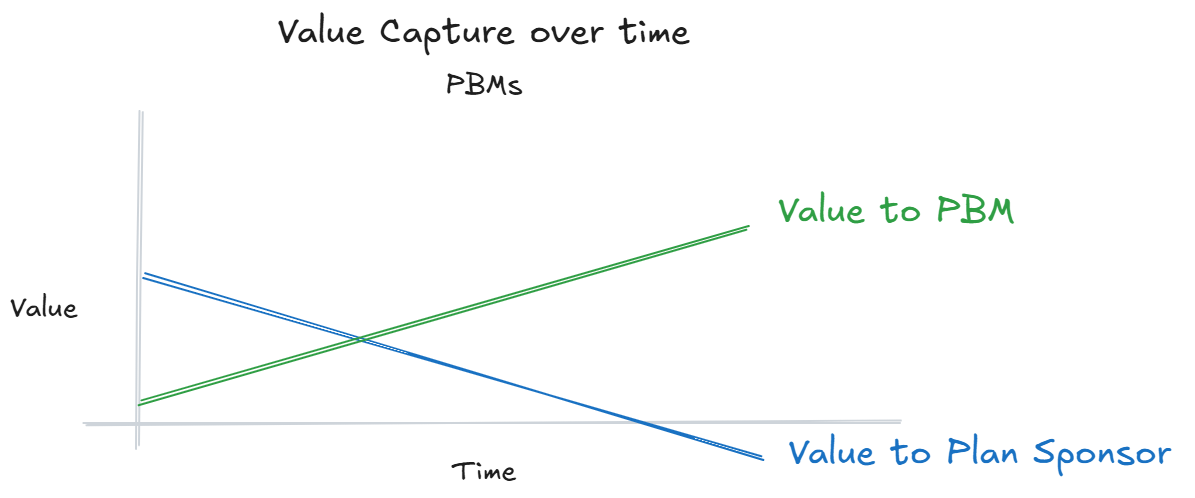

Pharmacy Benefit Managers

PBMs are the most obvious aggregators in healthcare. PBMs started in the 1960’s to process claims, manage drug formularies, and create a network of pharmacies. In the 70s, PBMs adopted electronic adjudication of claims. In the ‘90s, pharmaceutical manufacturers acquired PBMs in order to ensure their access to patients (Merck acquired Medco in ‘93). Prior to the 90s, PBMs had little power and low margins. They built the payment rails and protocols to connect a multi-sided network of patients, plan sponsors, insurance companies, and retail pharmacies. In the 2000s, insurance companies acquired PBMs and vertically integrated their services into their health plans (OptumRx acquired Prescription Solutions in ‘05 and rebranded it to OptumRx in '11, CVS acquired Caremark in ‘07, and Cigna acquired ExpressScripts in '18). With the vertical integration came increased complexity and intercompany monetary transfers. In the past 10 years, all 3 big PBMs created offshore GPOs to funnel profits through. These offshore GPOs allow the PBMs to say they are transparent and pass 100% of rebates back to the plan sponsor because they can just keep their profits at the GPO.

PBMs create revenue for themselves from rebates, spread pricing, and data (DIR) fees. In the 80s and 90s, these fees were reasonable because the savings obtained from PBMs’ contracts outweighed the fees. However, their vertical integration and information asymmetry have allowed PBMs to capture more and more value from the pharmaceutical supply chain to the point that plan sponsors are questioning the value of these PBMs. For more information on PBMs' subterfuge, I recommend reading the FTC’s report. As a result of the PBMs’ business behavior, Eli Lilly and Novo-Nordick are now offering direct pharmacy sales to patients. Eli Lilly recently cancelled their employee benefits with Express Scripts in favor of an independent, transparent PBM.

Quality used as a negotiating tactic

In the 70s and 80s, PBMs started drug formularies based on quality. PBMs realized they had substantial purchasing power when they selected their preferred medications for their formularies. When similar quality medications were available to treat a specific disease, PBMs could demand larger rebates. Whichever manufacturer agreed to the largest rebate would be named as the high-quality medication. Mark Cuban has recommended that the PBMs should separate their formularies from the PBMs. PBMs should not be able to manipulate the perceived quality of a medication to extract a larger rebate.

Fortunately, aggregators rely on third-party physician-rating companies like Embold Health and GAM to determine high-quality physicians, and out-of-network providers are not considered low-quality providers. It is imperative the physician quality ratings remain separate from the pricing negotiations.

How you get paid matters

Plan sponsors are beginning to realize that you cannot set third-party fees relative to variables that are controlled by the third-party. Buying a shirt on sale for 50% off is still a poor deal if the retail price of the shirt was tripled before the sale started. Plan sponsors have learned that you cannot value a network by the network’s percent discount off the chargemaster list because the networks have encouraged the providers/hospitals to increase their chargemaster rate so their network looks more attractive. Plan sponsors have learned that you cannot evaluate a PBM by the PBM’s rebates because the PBMs have encouraged the pharmaceutical companies to increase both their prices and rebates. Plan sponsors will need to realize that the reference price for surgical bundles needs to be the most competitive price available in the patient’s vicinity.

My predictions for the future

Aggregators will follow the PBM playbook. Aggregators will develop the complicated processes so they become integral in surgical bundle transactions. They will then attempt to inflate the reference price so they can show more savings on paper. They will continue to put pricing pressure on provider organizations and add data, credentialing, and care navigation fees.

BUCAs will try to acquire Lantern, Carrum, and/or Transcarent so the carrier can vertically integrate these aggregators into their existing networks. This would allow the BUCAs to generate revenue on surgical bundles that would be counted as medical care towards their medical loss ratio but that would ultimately flow back to the organization. The FTC can not allow any more vertical integration mergers in healthcare.

Aggregators are currently better at care navigation than marketplaces, but aggregators will need to move up the funnel and direct patients to the appropriate provider at the patient’s beginning of their MSK journey. Marketplaces will need to stop being passive and actively route patients to the preferred providers with care navigation, tiered networks, and first-dollar coverage. Carrum,

Aggregators are an easier business model to start, but I think the price transparency and aligned business interests of marketplaces will ultimately allow marketplaces to provide a better patient experience than aggregators, which should be the difference in the long run.